The Collapse of the Middle Class

The Collapse of the Middle Class Last week, I covered why the cost of housing is so expensive. One of the reasons is that the average American’s wage rate has not kept up with inflation or the cost of housing. Since the start of the pandemic in March 2020, over 1 trillion dollars in wealth has evaporated for working Americans. Over the last three years, many people in the US have experienced a collapse in their standard of living.

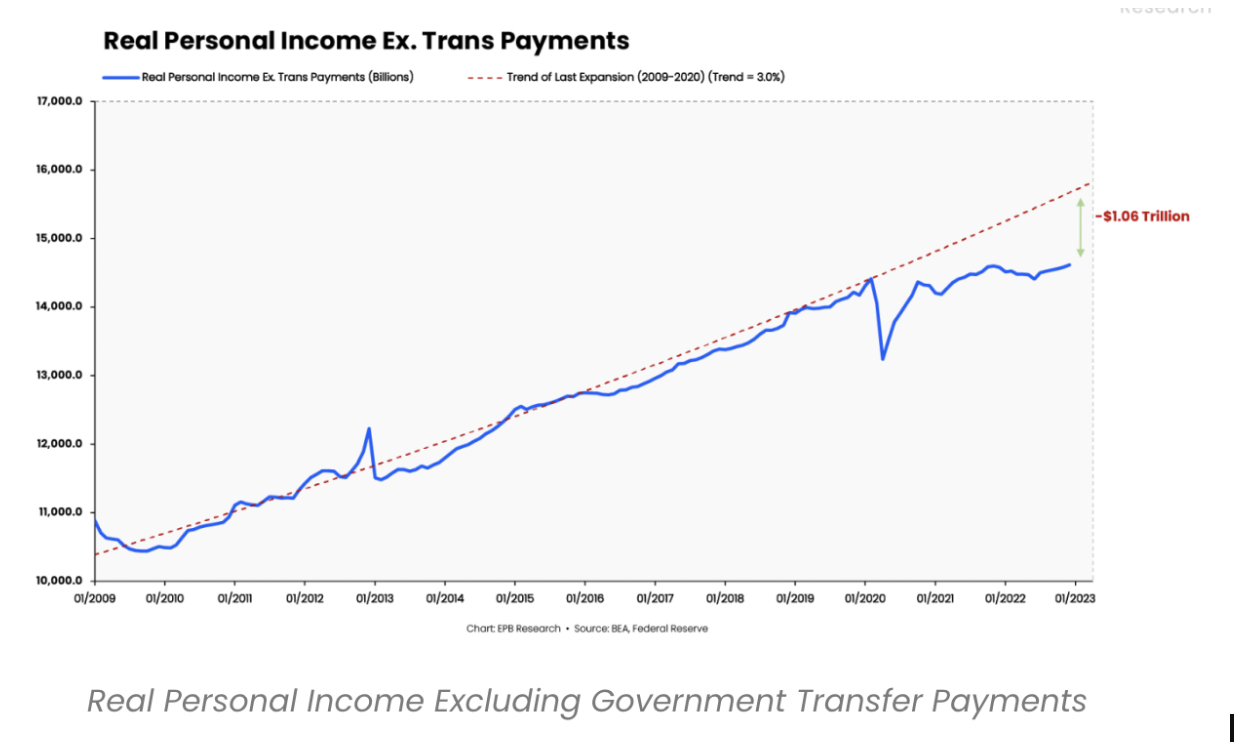

Private Sector Growth During that time, private sector income increased by only .5%. Since the 2009 housing crash, the private sector has seen a steady increase in real wage growth of 3%. Americans collectively would have earned more than one trillion dollars in real purchasing power since the pandemic if the trend had continued. This massive gap between what actually happened after the pandemic and what many people were accustomed to since the 2009 Great Recession is why so many people feel as though they are falling behind and struggling to maintain their previous lifestyle. Government subsidies have helped many people avoid financial disaster in the last 3 years. But those government transfer payments have mostly ended, and many Americans are shifting to having to rely on credit cards to make payments for basic needs. The decline in the standard of living for Americans is not unique to the pandemic. In fact, this is a trend that has been developing for over two decades.

Since 2001, real income growth has been declining, eroding the purchasing power of average workers. When measuring income for each economic cycle going back to the 1950s, the private sector saw real income gains of 3.3% from 1960 through 2007. From 2007 through 2023, real income has increased at half the historical pace of just 1.7%. Even at a modest inflation rate of 2%, wage growth has not kept pace with inflation. With inflation sitting at 9.5% in 2022, our buying power is far behind. Public and Private Debt Level A major change happened after the 2001 dotcom bubble. Between 2001 and the 2008 housing crash, recessionary income growth did not exceed 2%. After the COVID pandemic, we are down to less than one percent of real income growth. Furthermore, since 2001, the level of debt in the economy has increased. The added debt burden has strangled the capacity for new investments.

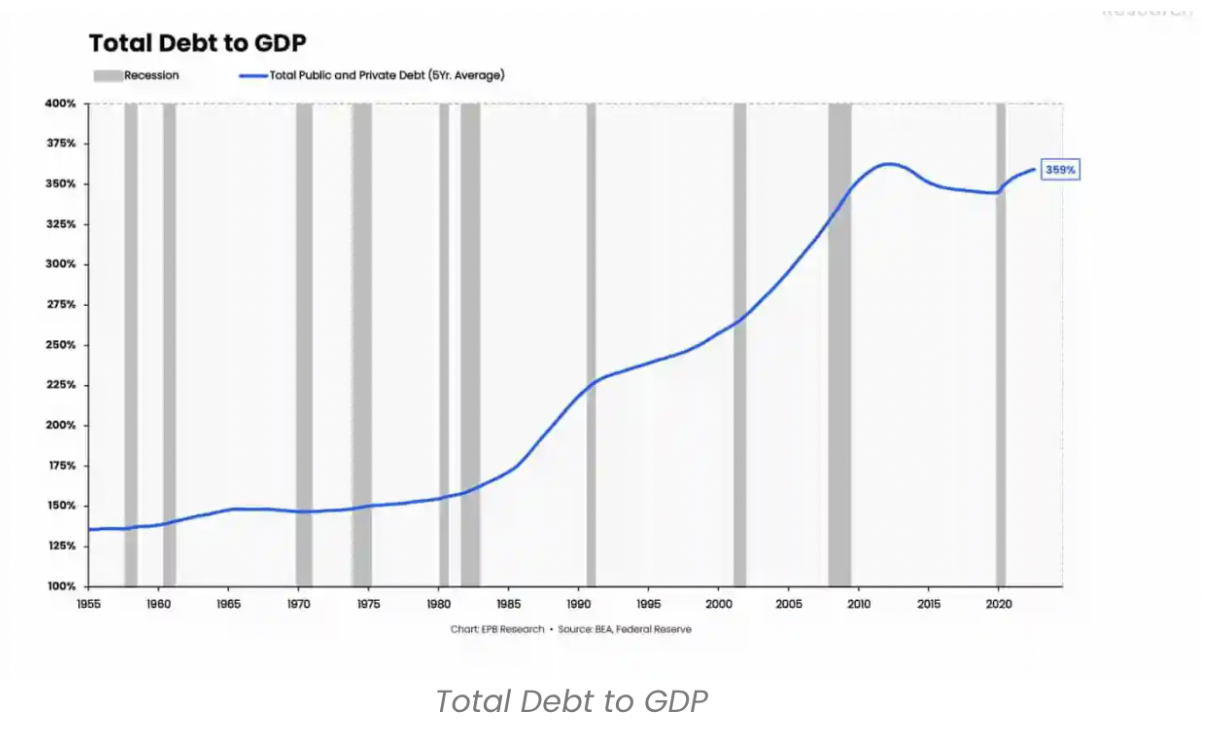

The total amount of public and private debt in the United States is 3.5 times bigger than the gross domestic product (GDP) of the whole country. Dr. Lacey Hunt, an economist, has done a lot of research on this topic and thinks that the ratio of debt to GDP should not be more than 2.75. Beyond this threshold, the economy starts to weaken dramatically. The U.S. crossed this critical threshold after the 2000s recession, which is why the private sector’s ability to generate income growth collapsed during the same time. The excessive indebtedness of the public and private sectors has severely weakened the economy. The subsequent response to the pandemic of adding even more debt has only added to our country’s growing debt. Government Spending The growing size of government spending as a share of GDP is another problem that is affecting the private sector more and more.

This is an analysis of data using total government spending as a measure rather than a political viewpoint on the function of government. The size of government spending has increased from about 26 percent of the economy to almost 36 percent of the economy. Economists Andreas Berg and Magnus Henriksen think that a government spending increase of this size slows real economic growth by 0.5% to 1%. Research also shows that increasing the size of the government can help in the short term. For example, going from spending nothing on government to spending 15% can lead to social benefits and better growth. But it is clear that when the size of government spending goes above 25% and gets close to 35%, the huge amount of money spent by the government hurts the private sector.

The growing levels of debt and an increase in public spending do not paint a rosy picture for future economic growth. The sins of the past are weighing down the private sector and are directly impacting everyday, average Americans like you and me. Forecast of Future Pressure Barring some very dramatic changes in our culture and political scenario, I don’t see a near-term path of change. The forces at play are not helping the average American gain financially. I see a slow but gradual economic squeeze of the middle class. I suspect you are personally feeling this pressure, too. So, while I hope regulators, policymakers, and economists can all agree on how to address these macroeconomic forces, I believe a significant change in that trajectory is unrealistic. How to Improve Your Station What is an individual investor left to do? My suggestion is to not rely on third parties to provide your income and to wait for raises that create more buying power. You have to take matters into your own hands.

Over the same time period, asset values have grown much faster than income. So we all need to think differently than normal wage earners. We need to become business owners that are creating value or real estate investors that hold appreciating assets that provide cash flow instead of solely relying on a wage to cover our needs. Becoming a business owner or real estate investor will not only help you keep up with the rising cost of living but can also create a foundation on which to build your financial future. This means that, rather than just relying on an employer to pay you a salary, you can take proactive steps to ensure your financial security Wishing you all the best! Paul.